Homeownership remains one of the most powerful drivers of generational wealth—but it’s become a marathon, not a sprint.

This shifting timeline and the long-term reality of building equity were the central focus of a recent panel discussion at the Realtor.com® 2026 SXSW Open House.

“I like to think of housing … not as a get rich quick scheme, but as a get rich slow scheme,” Danielle Hale, chief economist at Realtor.com® said.

It may sound like an underwhelming marketing pitch at face value, but the results speak for themselves.

The typical homeowner boasts a net worth of nearly $430,000, while the typical renter’s net worth sits closer to $10,000, noted panelist Jessica Lautz, the deputy chief economist and vice president of research at the National Association of Realtors.

That disparity has grown in recent decades: The median wealth gap between renters an owners increased 70% since 1989, while the average wealth gap ballooned 260%, according to Jung Hyun Choi, a principal research associate in the Housing Finance Policy Center at the Urban Institute.

But the ‘get rich slow’ race only works if people can actually get to the starting line. To that end, the panelists agreed that addressing the housing shortage is the only way to ensure that homeownership remains a viable pathway to wealth for all.

‘You can’t inherit your rent’

Behind those staggering differences in net worth is a simple fact: While rent is an expense, homeownership is an asset.

Colin Allen, Executive Director of the American Property Owners Alliance and the discussion’s moderator, put it more bluntly: “You can’t inherit your rent.”

As homeowners pay down their mortgage principal month-by-month, and their property gains value year-over-year, they gain equity. So even if a homeowner doesn’t feel financially different than they did as a renter, they are quietly performing the work of wealth building.

Renters don’t benefit from any such mechanism, despite carrying a monthly housing expense just as owners do.

Breaking out of that cycle early can have outsized impact on a homeowners net worth. Buying your first home by age 32 associated with a 22.5% higher net worth (the equivalent of $119,000) at age 50 than buying just 10 years later, according to research from Realtor.com.

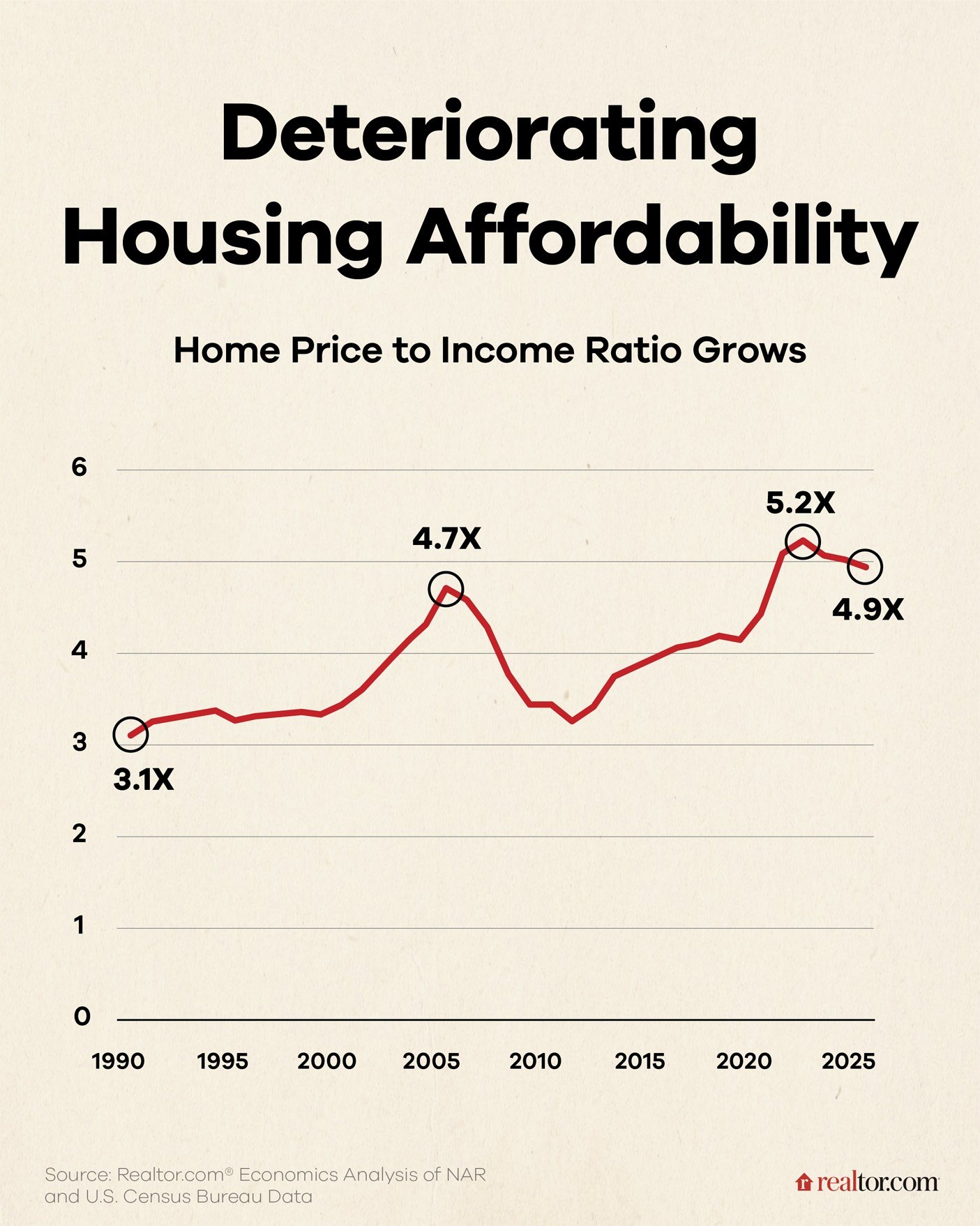

But getting into that first home has become harder to do. The median age of first-time homebuyers has climbed from 30 in 1990 to 40 in 2025, data from NAR shows. That shift has largely been driven by home prices rising nearly twice as fast as incomes—a deterioration that can be visualized by charting the ratio of home price to income, as seen below.

During this period, the time it takes the typical buyer to save for a down payment also ballooned from just over three years in 1990, to nearly ten years today, according to the report from Realtor.com.

Different starting lines

As the timeline to save for a down payment has gotten longer, more pressure has been put on family assistance to help buyers enter the market during that critical early window.

“One of the things that we find is that housing facilitates generational wealth, and children of homeowners are far more likely to become a homeowner themselves by age 35,” Hale noted.

This “stickiness” of homeownership—where the success of one generation dictates the opportunities of the next—has resulted in staggering gaps when paired with systemic barriers to mortgage and credit access.

“White Americans have a homeownership rate of 75% and African Americans and Hispanics are under 50%,” adds Hale.

“A lot of Hispanic or Black young adults don’t have a homeowner parent to help them purchase [their first] home with down payment support,” Choi explained.

Without that initial transfer of equity, these buyers are forced to navigate the market alone, often facing higher denial rates. Currently, debt-to-income (DTI) ratios are the number one reason for mortgage denials, a hurdle often exacerbated by the burden of student loans.

This creates a catch-22: To lower their DTI and keep monthly payments affordable in a high-rate environment, buyers need larger down payments—the very thing those without generational wealth struggle to provide.

Opportunities at the edges

But while it’s gotten harder to achieve, the get rich slow scheme still works.

“I don’t think that homeownership as a means of wealth building will go away,” Hale said.

While owners may face cash flow issues in the same way renters do, owners benefit from a level of housing cost certainty and foreclosure protections that renters just don’t have.

That added stability is why Choi thinks that responsibly expanding the credit box to help more homebuyers qualify is one way that could improve access to homeownership.

Lautz also highlighted looking to “the edges” of the market—innovations like accessory dwelling units (ADUs) and modular construction.

And while the barriers to entry are higher than they were for previous generations, the long-term payoff for those who can break through remains transformative.

In Hale’s words: “It’s not without challenges, but it is still really worthwhile.”

{kind=link}