Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Donald Trump wants average Americans to start investing in private credit. A couple of weeks ago, the president cleared away legal barriers to employers that want to let workers put their 401(k)-retirement money into riskier but potentially higher-yielding assets like private equity, real estate funds and so on. Big institutions and rich people do it, he says, so why shouldn’t everyone else?

I would argue that the government shouldn’t be encouraging average Americans to go into such alternative investments right now because we are likely entering the very tail-end of a risky credit cycle that could blow up. This isn’t a radical statement. It has become widely understood that, following the global financial crisis of 2008, risk moved from the formal banking sector into the private credit market. But to understand why this moment is so very delicate, it helps to go back further in history for lessons, to the junk bond crisis of 1989-90.

Former Biden administration Securities and Exchange Commission chair Gary Gensler, now a professor at MIT who teaches among other courses “Disrupting Wholesale Finance”, explains it thus.

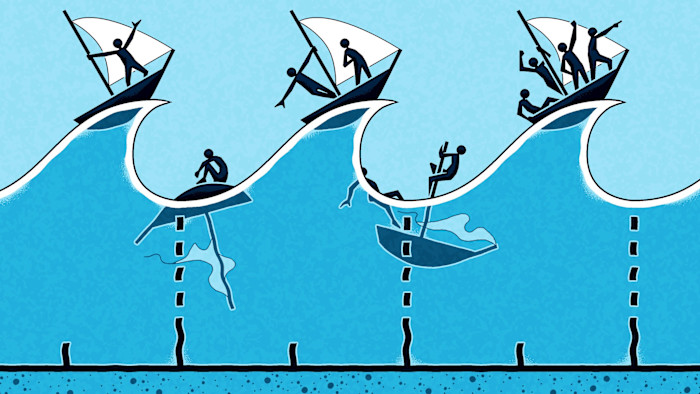

Levered lending credit cycles move in waves. For the past five decades or so, each wave has been about 15-20 years long. And each has had a transition point that was associated with a new kind of debt financing.

In every one of these cycles, Gensler says, “a fulcrum opens up gaps in the marketplace”. Financial innovators pile in, and incumbents begin to lose market share to new players who are doing new kinds of deals.

Start with the first wave: the leveraged buyout story, which began in the mid to late 1970s, when a small network of individual financiers like Henry Kravis, George Roberts, Thomas Lee, Teddy Forstmann and others developed the junk bond market. Fortunes were made and eventually lost amid the collapse of Drexel Burnham Lambert in 1990; the savings and loan crisis that stretched into the mid-1990s; the recession of 1990-91, and a Gulf war that — interestingly, given what’s happening now in Iran — coincided with that slowdown.

After that bubble burst, there was eventually a second wave of debt financing, based not on individuals doing specific deals, but rather on emerging alternative investment platforms like Blackstone and Carlyle that didn’t depend on a single star player. These institutions built “platforms”, as Gensler puts it, that could invest in more sectors and assets at any given time, raising far more money.

Some of the largest institutions eventually took their management companies public (Blackstone did an IPO in 2007), which in turn created more pressure for them to keep growing to please shareholders. This wave coincided with the development of broadly syndicated loans, collateralised loan obligations, and a tech boom. It ended — roughly two decades later — with the global financial crisis, which was of course housing related but amplified by leverage in the CLO market.

The third wave — the one we are in right now, which began right after the financial crisis — is about the rise of private credit as an asset class that is now held by pension funds, college endowments, family offices, and increasingly, insurance companies and high-net-worth individuals. We are now nearly two decades into this wave, which happens to coincide with both a tech bubble and a war in the Middle East.

“As Mark Twain purportedly said,” Gensler concludes, “‘history may not repeat itself, but it often rhymes.’” True enough. There is an argument that the structure of private credit is different today than in the LBO era, for example, with gates and closed-end funds, and that trouble in the market would not necessarily be systemic.

Whether that’s true or not, private capital firms are looking to juice the credit boom further by opening the $10tn US 401(k) market to riskier alternative assets. And Trump, who wants the market up at all costs, intends to help them do that.

The question for investors and policymakers who care about average Americans is this: are average retirees poised to be the “slow deer”, as the old Wall Street argot has it, of this late-stage credit cycle? In other words, are they the less sophisticated market participants who get eaten?

I think the answer is yes. Warning signs about the risks of levered lending, which has worked its way deep into the financial system, are high. There is ample evidence that private levered loans are trading well below par. Funds are increasingly repacking ageing assets and trying to offload them in the burgeoning secondary market. Experts from Jamie Dimon to Jerome Powell have been pointing out the risks in the private credit markets for some time, and the dangers they pose to the financial system and real economy. Even Trump’s own Treasury department is talking to state insurance commissioners about the private loans piling up on their portfolios.

There’s no question we are at the tail-end of another private credit cycle. The only question is how it ends, and who gets hurt. When the junk bond market collapsed, it was worth a little over 3 per cent of the entire US economy at the time. Today, private credit is about $2tn, more than double that figure as a percentage of the US economy. Add to that global conflict, energy inflation and an AI bubble. Slow deer, beware.

Join FT journalists for a subscriber webinar on April 16 about Private credit: how worried should we be? Register at ft.com/credit

{kind=link}