Keep knowledgeable with free updates

Merely signal as much as the Property sector myFT Digest — delivered on to your inbox.

The Federal Reserve may not have truly minimize rates of interest but, however so far as US housing is anxious, the fabled pivot has already began. And it’s seismic.

With the 30-year Treasury yield sliding from a excessive of over 5 per cent final October to just about 4 per cent this month, US mortgage charges have tumbled from practically 8 per cent to about 6.5 per cent.

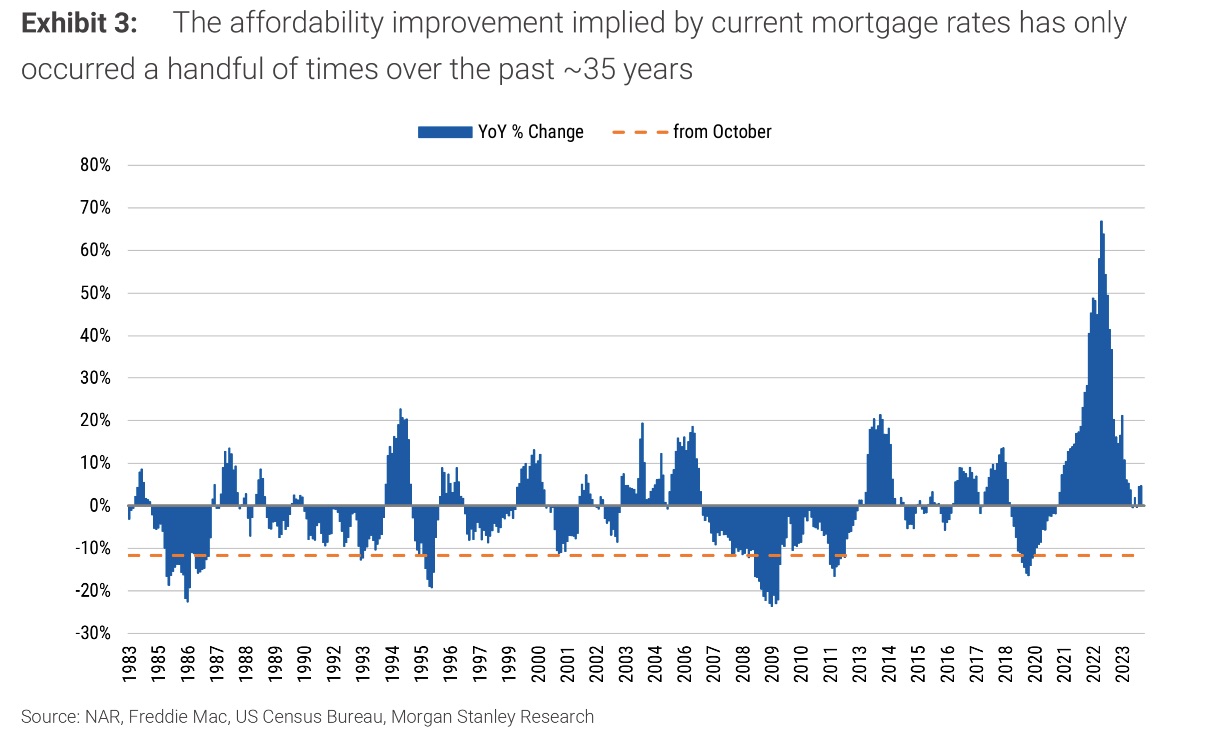

That is likely one of the largest enhancements in affordability previously 4 many years, in response to Morgan Stanley, and doubtless the most important mortgage fee whiplash in historical past (zoomable version):

So what does this imply for the weird, comatose US housing market?

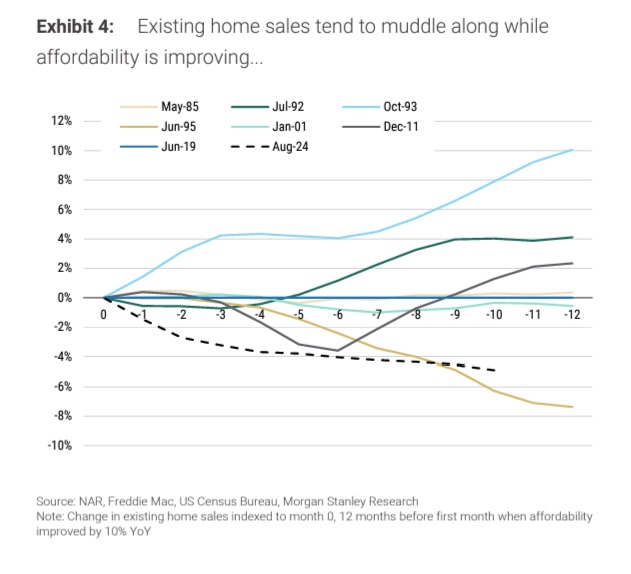

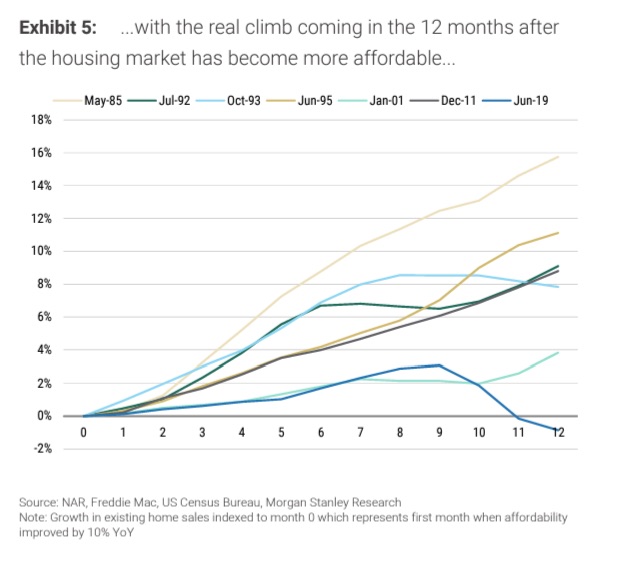

Morgan Stanley regarded on the different time when affordability improved by 10 share factors or extra, and located that house gross sales have a tendency to stay sluggish for some time, earlier than selecting up briskly over the subsequent 12–24 months.

(Left and right zoomable variations.)

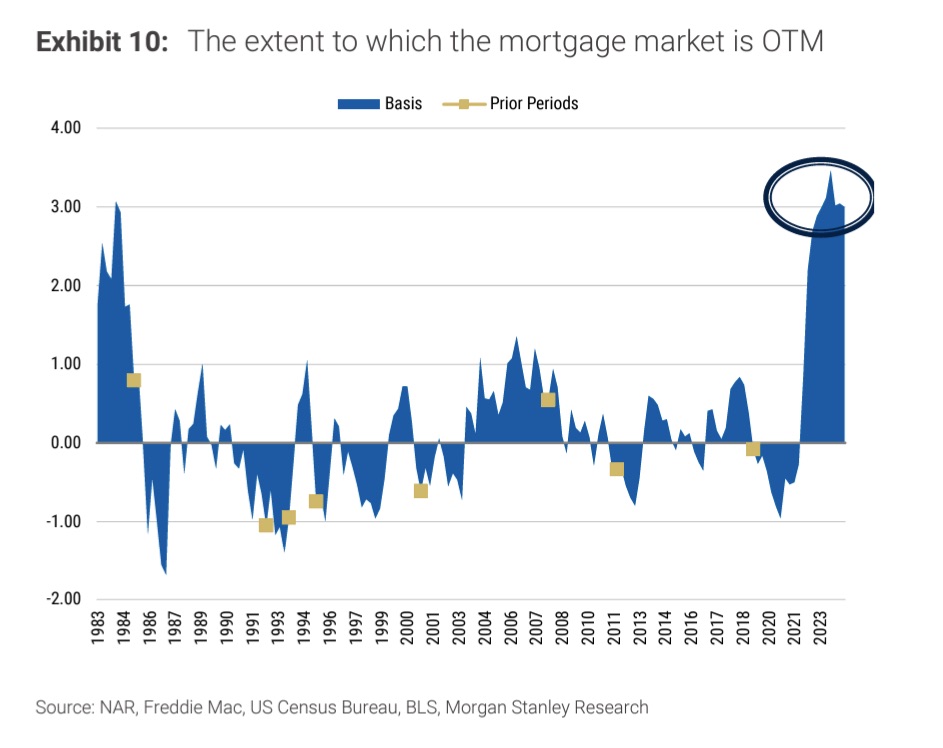

Nonetheless, as you possibly can see from the above chart to the left, we’re at the moment monitoring significantly under the norm.

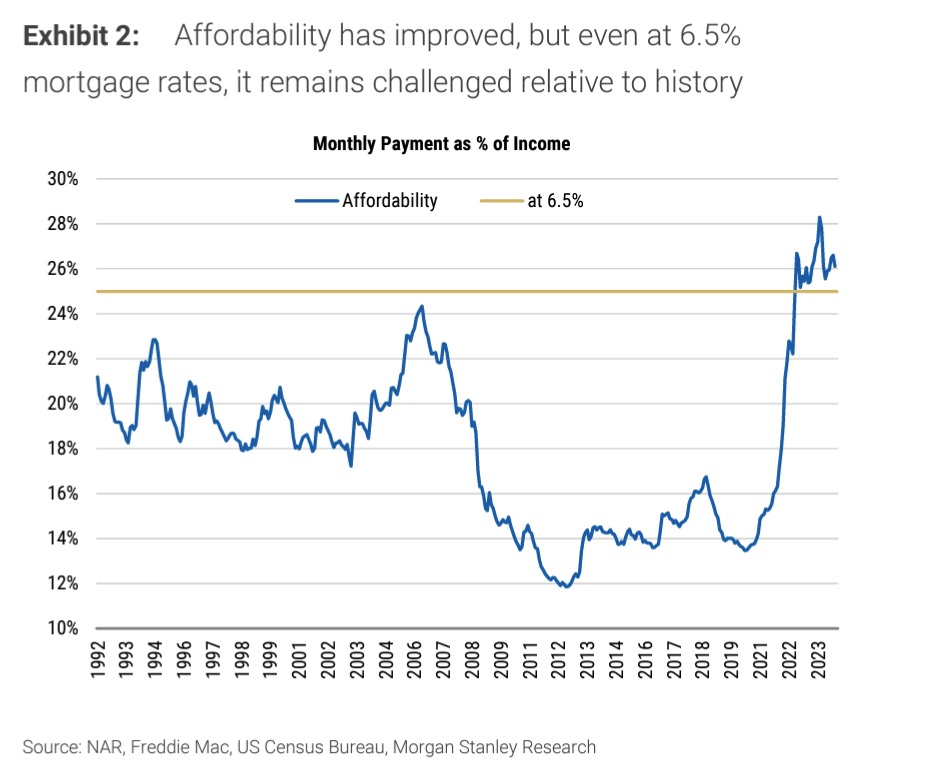

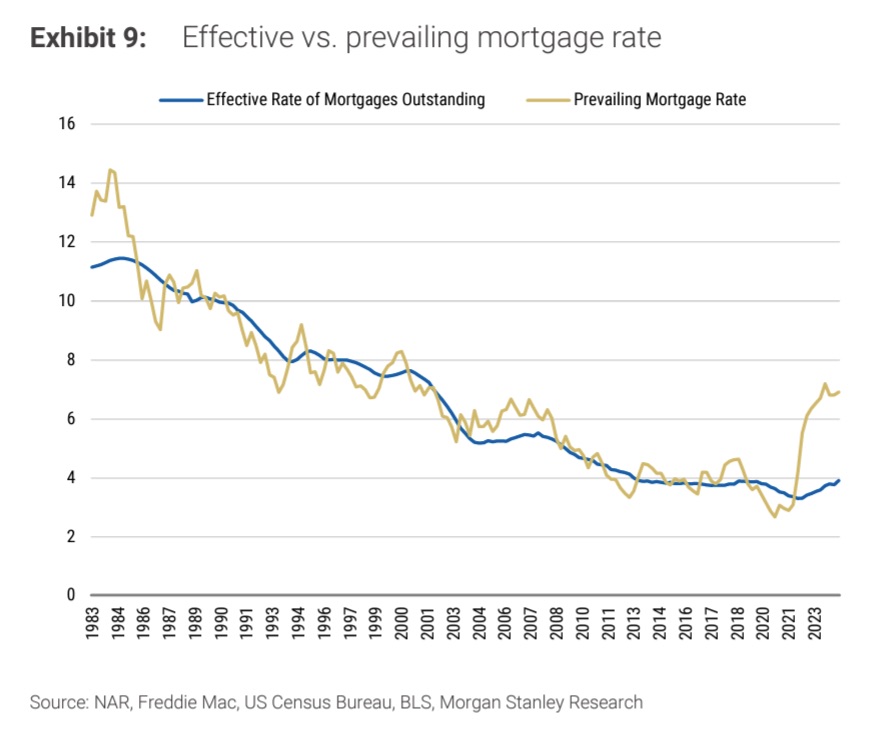

That’s virtually definitely as a result of the affordability of US mortgages stays fairly unhealthy even after the latest enchancment (zoomable version):

For those who’re residing in a home with a long run mounted fee mortgage that prices 3-4 per cent, shifting and resetting to over 6 per cent remains to be an enormous ask, even when it isn’t as unhealthy as resetting to 7–8 per cent.

And Morgan Stanley estimates that the hole between the present mortgage fee and what the typical US family is at the moment truly paying for his or her mortgage is the best since at the very least the early Eighties.

Which is why the US housing market will most likely stay in near-stasis till the traditional 30-year mounted mortgage fee drop a LOT decrease. As Morgan Stanley’s economists conclude:

When trying completely at prior durations of great affordability enchancment, it could appear to recommend that current house gross sales may improve at a wholesome clip within the subsequent couple of years. Nonetheless, upon a more in-depth take a look at the overlapping narratives regarding the extent to which owners are locked in, how unaffordable the housing market is in the present day, and the way few houses can be found on the market, evidently current house gross sales volumes are preventing extra of an uphill battle in the present day.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}